The 2026 Federal Budget Just Changed the Rules for Property Investors

Negative gearing, CGT reform, and what investors need to understand before making their next move

Last night, Treasurer Jim Chalmers confirmed the most significant proposed changes to property investment taxation since 1999. For over 25 years, investors have relied on two core tax settings: the ability to deduct rental losses against salary income, and the 50% capital gains tax discount for assets held longer than 12 months.

The 2026–27 Federal Budget, handed down on 12 May 2026, begins the process of unwinding both. Understanding what is changing, what is staying the same, and when each change takes effect is now essential for both existing and future property investors.

Important context before reading further

These are proposed Budget measures and remain subject to formal legislation. The key date triggering most negative gearing changes is 7:30pm AEST on 12 May 2026, being Budget night.

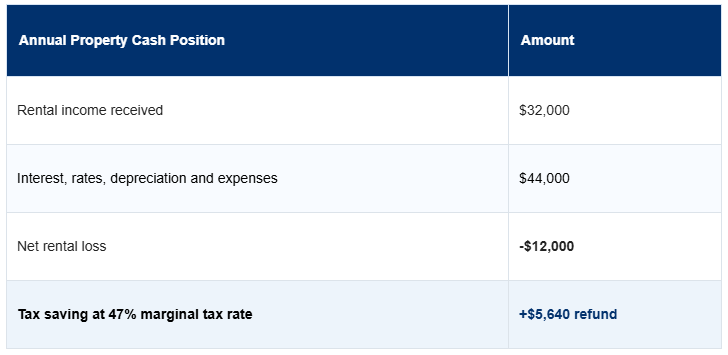

What Is Negative Gearing and How Does It Work?

Negative gearing occurs when your investment property costs more to hold than it earns in rent. The shortfall — your net rental loss — can currently be deducted against your other income, including salary or business income.

That annual refund has long been a meaningful contributor to holding costs. Over five years, it represents more than $28,000 in cumulative tax savings, which many investors use to reduce debt, fund renovations, or prepare for their next acquisition.

What Exactly Is Changing?

There are two major reform pillars in this Budget. Both are proposed to take full effect from 1 July 2027, while the negative gearing changes are triggered from Budget night.

1. Negative gearing — restricted for established properties

From 1 July 2027, investors who purchased an established residential property after 7:30pm on Budget night will no longer be able to offset rental losses against salary or wage income. Instead, losses must be carried forward and applied against future rental income or capital gains from residential property.

Good news for existing investors

If you already own an investment property, or had a contract signed before 7:30pm on 12 May 2026, you are expected to be grandfathered. Your current negative gearing deductions continue unchanged until you sell.

2. Capital gains tax — the 50% discount is being replaced

Currently, if you hold an investment for more than 12 months, only 50% of your capital gain is taxed. From 1 July 2027, this is proposed to be replaced with a cost base indexation methodology and a 30% minimum tax on net capital gains. This applies to all CGT assets, not just property.

Investors in new builds are expected to have the option to choose between the existing 50% CGT discount or the new indexation method, depending on which is more favourable at sale.

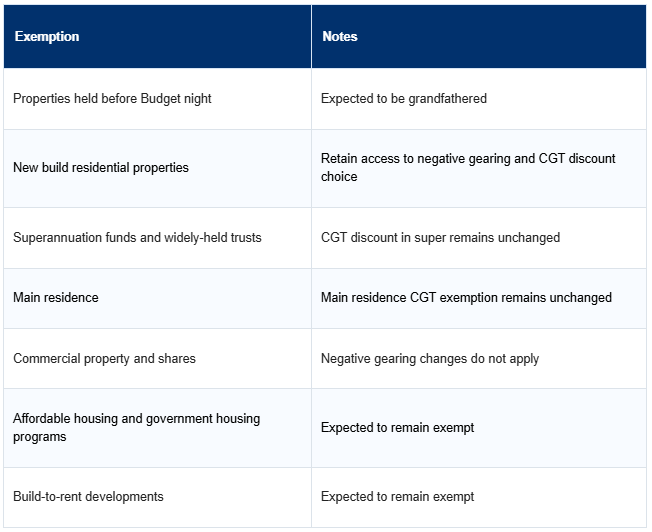

What Remains Exempt?

When Does Each Change Take Effect?

Established Property vs New Build: The New Reality

The reforms create a clear and deliberate distinction in after-tax outcomes between established properties purchased after Budget night and qualifying new builds.

Established Property (Post Budget Night)

Changed Position

| . | Negative gearing against salary: restricted from 1 July 2027 |

| . | Annual tax refund on rental loss: no longer available |

| . | Losses carried forward against rental income only |

| . | 50% CGT discount: replaced with indexation + 30% min tax |

| . | Tax efficiency vs. new build: lower |

New Build (All Purchases)

Preferred Position

| . | Negative gearing against salary: fully retained |

| . | Annual tax refund on rental loss: continues |

| . | Choice of 50% CGT discount OR new indexation method |

| . | CGT: choose whichever is more advantageous at sale |

| . | Tax efficiency vs. established: higher |

The tax advantages of property investment are not being eliminated — they are being deliberately redirected toward new housing supply.

What Counts as a New Build?

Full legislative detail is yet to be released, but based on current government commentary and prior policy frameworks, the following provides a working guide.

How Should Investors Think About This?

Rather than viewing these changes purely as a threat, sophisticated investors should recognise them as a recalibration — one that rewards those who adapt their strategy early and focus on asset selection, cash flow and long-term tax planning.

Key Takeaways

If you own investment property today, your existing holdings are expected to be grandfathered.

Established properties purchased after 7:30pm on 12 May 2026 will face restricted negative gearing from 1 July 2027.

The 50% CGT discount is proposed to be replaced from 1 July 2027, although new builds may retain a more favourable choice.

Rental losses are not necessarily lost; they may be deferred and carried forward against future property income or gains.

Detailed legislation and transitional rules are still to come, so investors should avoid irreversible decisions based solely on Budget commentary.

Equimax Property Investment Advisors