Sentiment vs. Fundamentals

Why Australia’s Property Market Remains Structurally Resilient

Global geopolitical uncertainty, persistent cost-of-living pressures, and a cash rate now sitting at 4.10% have collectively weighed on investor sentiment. Yet the most recent Cotality Home Value Index confirms national dwelling values rose 9.9% over the past year, with 11 of 17 geographic segments at all-time peak values.

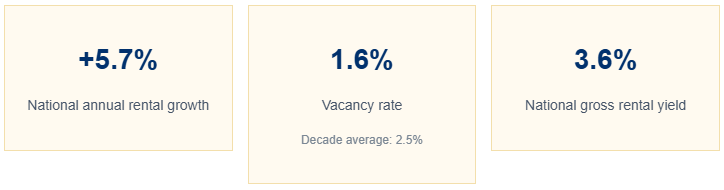

The labour market remains a structural stabiliser: 14.7 million Australians are employed, the unemployment rate sits at 4.2%, and national rental vacancy is just 1.6% — well below the decade average of 2.5%. The picture is one of a market under sentiment pressure, but not structural impairment.

Three Headwinds Shaping Sentiment

Three macro forces are measurably weighing on buyer confidence and market activity. Understanding each one is essential to separating the noise from the signal.

Global Geopolitical Unrest

Geopolitical risks have intensified sharply in 2026. US–China trade competition, the ongoing Middle East conflict, and broader global fragmentation have pushed energy prices higher, disrupted supply chains, and eroded consumer and investor confidence in ways that extend well beyond financial markets.

For Australian property investors, geopolitical uncertainty operates primarily through sentiment channels — compressing buyer urgency, elevating decision paralysis, and softening auction clearance rates. These are real, measurable effects, but they do not alter the structural supply-demand position of the market.

Cost-of-Living Pressures

CPI is running at 3.7% annually, still above the RBA’s 2–3% target band. Wage growth has not kept pace with inflation in real terms, placing sustained pressure on household discretionary spending. Higher energy prices are adding a compounding layer of cost pressure for mortgage-holding households.

Cotality data shows this is most consequential at the premium end of the market. In Sydney, upper quartile values fell 1.8% through Q1 2026, while lower quartile values rose 1.8% — a 3.6 percentage point spread. Affordability constraints are not contracting the market uniformly; they are reshaping where demand concentrates.

Source: Reserve Bank of Australia, rba.gov.au — Cash Rate Target effective 18 March 2026

March 2026: What the Data Shows

The Cotality Hedonic Home Value Index released its March 2026 results on 1 May 2026. The national median dwelling value now stands at $933,137.

Source: Cotality Home Value Index, results as at 31 March 2026

The Two-Speed Market in Sharp Relief

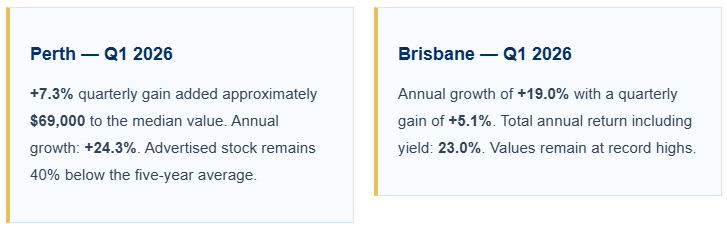

Sydney and Melbourne are navigating the early stages of a downturn. Perth, Brisbane, Adelaide and Darwin are breaking record highs. Perth’s advertised stock is tracking approximately 40% below the five-year seasonal average — a supply constraint that continues to support price growth even at a cash rate of 4.10%.

11 of 17 geographic segments tracked by Cotality are currently at all-time peak values. This is not the profile of a market in broad structural retreat.

Rental Markets — A Structural Supply Crisis

Every capital city is recording a vacancy rate below 2.0%. Adelaide is the tightest at 0.9%, followed by Perth at 1.1%. The quarterly rental change of 2.1% was the largest three-month gain since May 2024.

Source: Cotality Home Value Index, Gross Rental Yields and Annual Rent Growth to March 2026

Resilience in the Australian Property Market

Sentiment cycles. Fundamentals are slower to change. Three structural dynamics continue to underpin the resilience of Australian residential property.

Chronic Undersupply

Australia requires approximately 240,000 new homes per year to keep pace with demand and is currently falling around 60,000 homes short each year. KPMG projects the national housing shortage could double to 400,000 by 2028–29.

Population-Driven Demand

Australia’s population grew by 423,600 in the year to September 2025, with 2.98 million temporary visa holders as at 1 January 2026 — a record high. New arrivals enter the rental market first, sustaining vacancy tightness and supporting ongoing rental demand.

A Labour Market That Holds the Floor

ABS Labour Force data for February 2026 confirms the employment market remains structurally robust. The unemployment rate sits at 4.2%, total employment reached 14,721,400, the participation rate is 66.8%, and the employment-to-population ratio is 64.0%.

Source: ABS Labour Force, Australia — February 2026 (released 19 March 2026)

Equimax Perspective

Our advisory approach is grounded in evidence. The following observations are derived directly from the data in this report.

Market Selection: Perth delivered +7.3% in a single quarter, while Melbourne recorded -0.6% over the same period. Investors aligned with markets where the supply deficit is deepest are operating in a fundamentally different risk-return environment.

Lower-Quartile Opportunity: Cotality confirms lower quartile markets are outperforming upper quartile segments across every major capital. In Sydney alone, the spread was 3.6 percentage points in Q1 2026.

Rental Income Floor: National vacancy remains at 1.6%, annual rental growth is 5.7%, and Darwin unit yields have reached 7.2%. In well-selected markets, yield-on-cost is improving as rents grow faster than values.

Labour Market Stability: With 14.7 million Australians employed and the unemployment rate at 4.2%, forced selling risk — the mechanism that turns sentiment softness into structural decline — remains off the table.

I know there is no shortage of noise in the market right now. Yes, rates are higher than any of us would like. Yes, global headlines are unsettling. Yes, sentiment has softened — and that is showing up in some of the numbers.

But when I look at the full picture — 9.9% national growth in the past year, 14.7 million Australians in employment, vacancy rates near historic lows, and Perth delivering $69,000 of value growth in a single quarter — the structural investment case for well-selected Australian residential property remains as clear as I’ve seen it. The investors who stay disciplined, focus on fundamentals over headlines, and make data-backed decisions for long-term growth are consistently the ones who look back on these periods as the moments that defined their portfolios.

Equimax Property Investment Advisors